New fintech and paytech companies are created each day. Their sole reason to exist is to help the world by developing solutions that solve problems to consumers that legacy companies are (were) not able to capture in time, or at its best.

Strangely, one of the key concerns that these new companies have is how to scale themselves. And that is because they find bottlenecks in several processed when not tackled in the best way. Today we will focus on two of them: the onboarding of new clients, and KYC (know your customer) processes.

How much does it take to get a new user on board? Onboarding best practices

Do you remember how it was to open a bank account 5 or 10 years ago? You would need to fulfill – in a paper, of course – several forms, in many cases replicating the same information several times, sign them, and take them in person to a branch, where a human would receive the info, stamp it and send it to their internal onboarding team, who would read it, perhaps type some of its info into a computer (probably offline, or connected to an internal server at its best), finalize the process and send a paperback to the branch, where they would communicate by phone or in a paper letter that your account was granted. And that was just to open an account, taking a loan would imply significantly higher paperwork, time, effort, and money.

To scale up, fintech companies need to streamline their processes concerning Consumer Due Diligence (CDD) to avoid these legacy concepts being part of their spirit. For a ‘legacy’ company, instead, by looking at what fintech companies do, you need to understand that changing your old processes is only a matter of time. Their choice is: adapt or die.

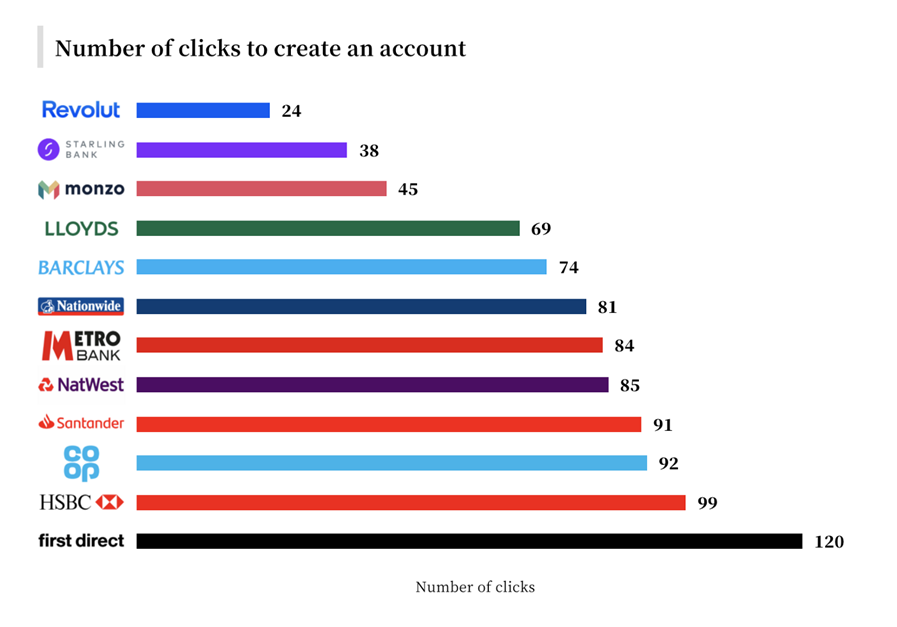

To scale up, fintech companies need to streamline their processes concerning Consumer Due Diligence (CDD) to avoid these legacy concepts being part of their spirit. For a ‘legacy’ company, instead, by looking at what fintech companies do, you need to understand that changing your old processes is only a matter of time. According to a study, it can take up to 5x more clicks to open a bank account in a legacy merchant versus the new banks, and 18x more time to have the accounts active. Their choice is: adapt or die.

KYC

How do we know who we are doing business with? As a company, we need to make sure all the regulatory and financial aspects are covered on the get-to-know your customer (KYC). This includes collecting specific information like the full name, phone numbers, national ID, passport, driver’s license amongst others. Also, from an Anti-Money Laundering (AML), to mitigate money laundering risks, as a company you should have well documented the origin of the sources of your consumers. But then the how to do it is key.

As a consumer, would you rather decide to do business with a company that requires you to show printed documents into a physical store, or would you rather prefer to do it within their website, their app, and get a confirmation in less than 24 hours?

The consumer journey and the user experience (UX) in this case are the drivers of success.

Let us help you

For many years, the team of GlobalTask is co-creating the future of financial technology by helping companies transform their financial services. With regards to the topics mentioned covered here, Onboarding and KYC transformation support is part of our core advisory values as a company, with a strong track record of expertise in this matter.

Let us help you, reach out to us here.